Approaching your 65th birthday and starting to receive a pile of letters about Medicare? Feeling lost? That’s normal. Medicare isn’t just one simple plan — it’s a system with several parts, dozens of options, and deadlines that cost you if missed. This guide will explain the most important things to you — simply and without the complications.

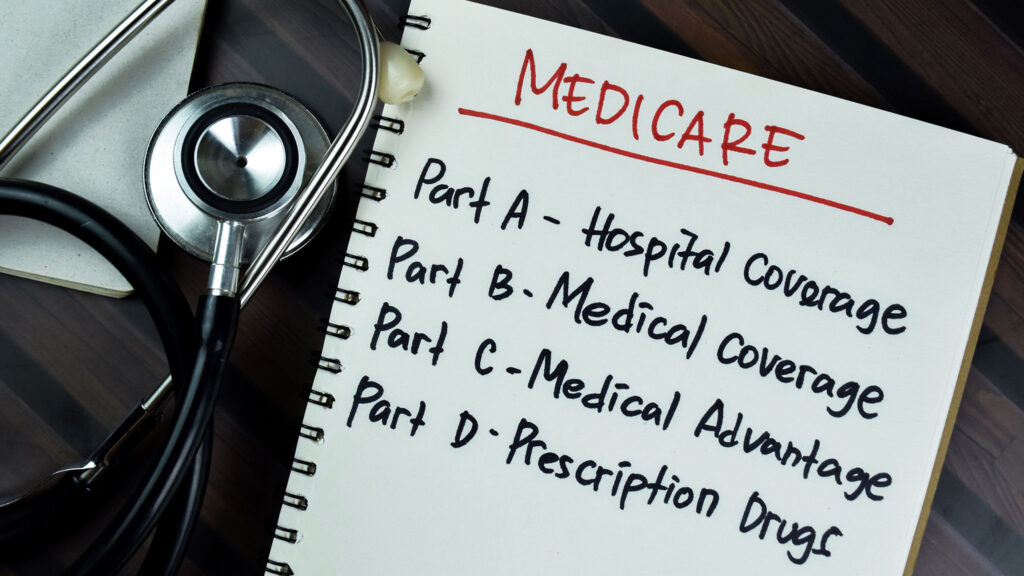

Medicare Parts — what covers what

- Part A (hospital) — most people get it for free if they worked in the U.S. for at least 10 years. It covers hospital stays, nursing care, and hospice.

- Part B (doctor visits) — covers doctor visits, preventive screenings, ambulance, and medical equipment. It costs money — the standard premium in 2025 is about $185/month, but it depends on your income.

- Part C (Medicare Advantage) — a private plan that combines Part A + B, often with extras (dentist, eye doctor, medications). Note: it limits your network of doctors.

- Part D (medications) — a separate plan for prescriptions. If you take regular medications, this choice has a huge financial impact.

Advantage vs. Supplement — the biggest dilemma

This is where people get lost. Medicare Advantage (Part C) is “all-in-one” — usually a lower premium, but a limited network of doctors and the need for referrals. Medigap (Supplement) is additional insurance that covers what basic Medicare doesn’t — copays, deductibles, and fees for longer hospital stays.

What does this mean in practice? If you have your own doctors and don’t want to change them — a Supplement gives you more freedom. If you are looking for a low premium and additional benefits — Advantage might be better. There is no single right answer. It depends on your situation.

Check out the Zimnoch Financial Group profile in the PolishPages directory

Deadlines that cost — literally

The Initial Enrollment Period begins 3 months before your 65th birthday and lasts for 7 months. If you don’t sign up for Part B during this window (and you don’t have insurance from work), you will pay a penalty — a 10% higher premium for every year of delay. For the rest of your life.

Many Poles on Long Island find out about this too late — for example, when they leave their jobs at age 67 and think that now they can “just sign up.” No.

What to look for when choosing a Medicare agent

- Do they compare many insurers? — an agent who sells only one company won’t show you better options from the competition. Look for a broker with access to many plans.

- Do they explain, rather than push? — a good agent will spend time explaining the differences. A bad one will say “this plan is the best” and tell you to sign.

- Service in Polish — Medicare is a complicated topic even in English. Terminology (deductible, copay, coinsurance, out-of-pocket max) is much easier to understand in Polish.

- Reminders about deadlines — an agent who calls before Open Enrollment and reminds you about plan changes is worth their weight in gold.

Zimnoch Financial Group meets these criteria — check out the profile in the PolishPages directory

Don’t risk penalties and bad plans. Call for a Medicare consultation: 631-760-7449